Is Wealth a Feminist Issue?

Better paying jobs aren’t enough to ensure women’s economic stability, according to a new study. For black women and Latinas in particular, a focus on bridging the “wealth gap” rather than the pay gap may make the most sense.

New research from Insight Center for Community Economic Development reveals disturbing data about a widening wealth gap in the United States, particularly in reference to women of color. While feminist organizers have long pursued fair and equitable wages, much more attention needs to be paid to the enormous disparity in wealth that undermines the future economic security of black and Latina women in particular. Insight's "Lifting As We Climb: Women of Color, Wealth, and America's Future" details this impending crisis.

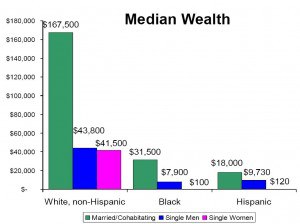

Wage equity is still a large problem for women—while the gender wage gap is widest for white women compared to white men, black, Latina, and Native American women take home far less than their white counterparts. But earnings are only a small part of overall financial stability. What matters more than income in the long run is the accumulation of wealth. As lead researcher Mariko Chang explains in her presentation summarizing the data, "wealth confers benefits income doesn’t." While income is vital for day to day survival, only wealth can generate further income, provide collateral for loans, be passed from generation to generation through inheritance, and provide the individual with the means to survive without a paycheck. Sadly, for many of women of color, the wealth gap is even wider than the income gap. Most women of color have no assets except for their cars—once the blue book value of the vehicle is removed from the calculation of median wealth, black women are left with a scant $100 in assets, while Latinas can only claim $120. The report explains: "To put it another way, single black and Hispanic women have one penny of wealth for every dollar of wealth owned by their male counterparts and a tiny fraction of a penny for every dollar of wealth owned by white women."

The wealth gap begins early. As might be expected, half of all young women, regardless of race, "are beginning their adult years with a median wealth of zero, meaning [they] had no wealth or had debts greater than the value of their assets." As they move into adulthood, such factors as rising school debt, family financial insecurity, less disposable income and the increasing use of credit cards to fund life essentials (like groceries and gas) inhibit wealth accumulation. As women of color continue along their career paths, more and more barriers to wealth building are encountered. In comparison, young men of all races tend to begin with a positive net worth, and maintain higher levels of wealth throughout their lifetimes.

Who Can Step onto the Wealth Escalator?

"Lifting as We Climb" coins a term, "the wealth escalator," to explain how various benefits designed to help the middle class tend to skip over black and Latina women. Such job related benefits as paid sick days, pensions and insurance enable people to amass a large amount of savings and disposable income, which can then be applied to investments and property that is then treated favorably in the tax code. However, our shifting corporate culture in America has seen an overall reduction in benefits like health insurance coverage, pension plans, and 401K contributions by companies, leaving women of color scrambling to cover these types of expenses out of pocket. Home ownership is another area in which black and Latina women lag behind their counterparts and are more likely to be pushed into a sub-prime mortgage: among single women, only 33 percent of black women and 28 percent of Latinas are homeowners compared to 57 percent of white women. The parenthood years are also fraught with peril as women of color are more likely to be supporting multiple children, as well as extended family, on their weaker salaries.

And not having opportunities to build wealth leaves women of color at a disadvantage in retirement. According to the report: "Women of color ages 65 and older are least likely to receive retirement income from pensions or from assets. For instance, while 49 percent of white men and 30.5 percent of white women receive income from pensions, 26 percent of black women, 17 percent of Asian women and 12.7 percent of Hispanic women receive any income from pensions. Likewise, whereas 66 percent of white men and 60.4 percent of white women receive income from assets, 40 percent of Asian women, 25.4 percent of black women, and 23 percent of Hispanic women receive any income from assets."

What Can Be Done?

The Insight Center recommends a variety of solutions to help bridge the wealth gap: improve opportunities for employment through targeted job training programs, ensure that government created jobs include fringe benefits and paid time off, strengthen unionization, set a higher wage standard for care positions, fund universal early childhood education programs to assist employed mothers, provide more benefits for the self-employed, remove penalties such as asset limits from government programs that work against women trying to climb out of poverty, and restructure the Social Security program through such measures as minimum benefits and adjustments for part-time workers. All of these recommendations focus on policy measures that would go far in reducing wealth inequality. Outside of the report's recommendations and guidelines for ending the wealth gap, another step to take would be launching an aggressive, feminist backed campaign to improve financial literacy and investment opportunities for women and girls. While feminists have already taken the lead on advocating for pay equity, other campaigns need to be launched in tandem. A renewed focus on advocating that more jobs include fringe benefits and health insurance would simultaneously stabilize more families and provide more disposable income through health care savings and pretax retirement deductions.

A campaign based around savings and investments should convince women of the necessity of having a savings account of one's own and how smart investments now can help provide a better future for their families. (Some one-third of single Latinas and one-fourth of single black women have no checking or savings account). This program should be designed with a cash-strapped individual in mind—many of the current programs based on savings and investment assume that women have a regular and reliable source of income, as well as thousands of free dollars to invest when many people are scraping by without the "latte and lunch" expenses financial experts ask people to cut.

"Lifting as We Climb" is a much needed wake-up call for activists and policy makers alike. As inequality continues to rise in the United States, direct action is needed to ensure that minority women are not left any further in the dust.

More articles by Category: Economy, Race/Ethnicity

More articles by Tag: African American, Equality, Working families